Reporting on Fraudulent Activities by Auditors

Introduction

Corporate Frauds!! The words doing rounds after India witnessed its own high-class corporate frauds from The Satyam, Commonwealth Games, 2G Spectrum or the Coal Gate Scam to the latest Nirav Modi Scam. Such scams put the entire country to shame, loose investors wealth, deprives Government of its tax revenues and even worse, puts the poor and deserving away from resources and support.

One of the measures that Government has taken is to ensure that such frauds are reported is by way of introduction of Section 143(12) in The Companies Act, 2013. While similar provision existed in the previous company law as well, 143(12) is more specific and action oriented. This section deals with the provisions on Reporting of Fraudulent Activities by the Statutory Auditor of the Company.

What is Fraud

There are 2 sets of Guidance to Statutory auditors on fraud reporting - Companies Act and Standards on Auditing. Let’s first understand the term fraud, which is defined in both The Companies Act, 2013 and the Standards on Auditing (SA).

The term fraud is defined u/s 447 – “Punishment of fraudâ€

Fraud includes:

a) Act;

b) omission;

c) concealment of any fact; or

d) This notification puts the following conditions for a start-up company to be exempt from angel tax:

e) abuse of position committed by any person or any other person with the connivance in any manner

f) with the intent to deceive,

g) To gain undue advantage from, or

h) to injure the interests of the company, its shareholders or its creditors or any other person whether or not there is any wrongful gain or wrongful loss.

Para 11(a) of SA 240 define fraud as - an intentional act by

a) One or more individuals among management, those charged with governance, employees, or third parties,

b) involving the use of deception

c) to obtain an unjust or illegal advantage.

There is a thin line of difference between the two definitions. Section 447 includes ‘acts with an intent to injure the interests of, the company or its shareholders or its creditors or any other person, whether or not there is any wrongful gain or wrongful loss’ whilst SA requires reporting when there is an act that have intent to injure the interests of the company and to obtain unjust or illegal advantage.

Reporting of Fraud by Auditor

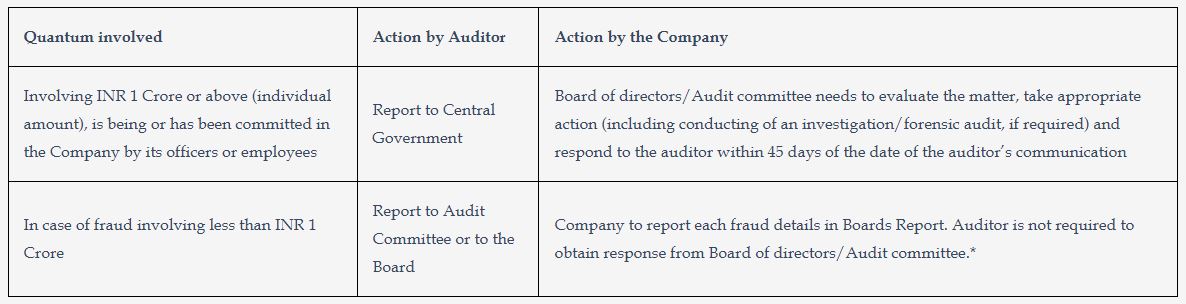

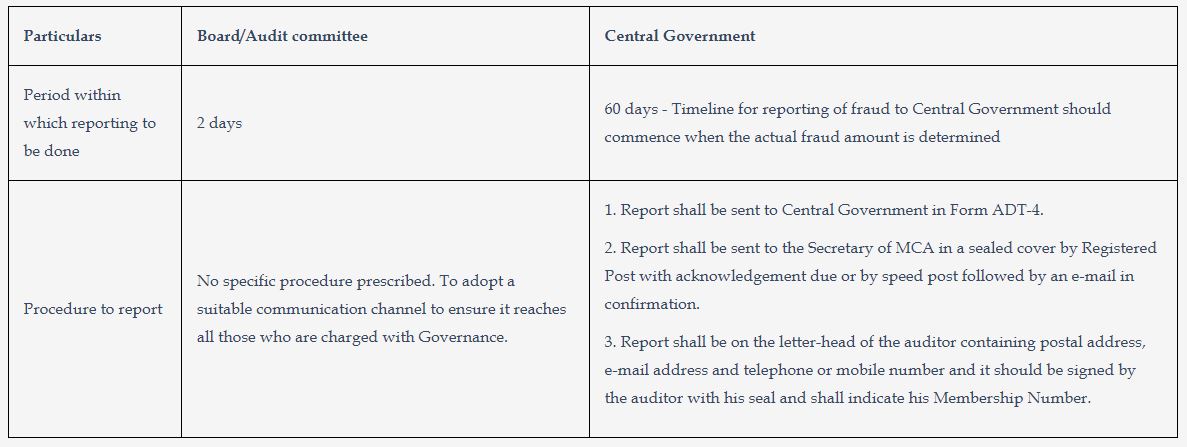

As per Section 143(12) of the Act if an auditor of a company in the course of the performance of his duties as auditor, has reason to believe that an offence of fraud has been committed by its officers or employees, the reporting of fraud is required as under:

Who needs to report on fraud?

A Statutory Auditor, Cost Accountant or a Company Secretary need to report on frauds. Though an internal auditor is appointed under the Act, fraud reporting doesn’t apply to them.

Reporting by auditors u/s 143(12) would apply even if the fraud is required to be or has been reported under any other statute or to any other regulating authority. For instance, a fraud detected is already reported by the auditor, appointed by the regulating statute for banking companies i.e. under the Banking Regulation Act, now the question is whether the statutory auditor can free himself from the provisions of this section saying the detected fraud is already reported and hence reporting under The Companies Act, 2013 is not required? The answer is No, since the section clearly tells reporting provisions would apply even if the fraud reported in any other act or under any other statute.

Manner of Reporting

The Manner of fraud reporting along with the response matrix is as under:

Punishment for Default

As per Section 147(2), if an auditor has contravened Section 143 knowingly or will fully with the intention to deceive the company or its shareholders or creditors or tax authorities the punishment for default would be as under: a) Punishable with imprisonment for a term up to 1 year and b) Fine which should be minimum INR 1 lac and can be further extended to INR 35lacs

Conclusion

With growing greed of people and morality dropping, Corporate frauds are raising. Auditor being the one entrusted with the responsibility to report on any such frauds, the role of auditor is rapidly changing and the expectation of Government and people at large are also increasing. Auditors need to equip themselves and their audit practices to detect any fraud that might have taken place, including frauds emanating out of use of technology, to not only report them to cover their legal responsibility but also to discharge their moral responsibility.